Chapter 12: Cooperatives

Cooperatives

When individuals join in a cooperative venture, the power generated far exceeds what they could have accomplished acting individually.

R. Buckminster Fuller

The cooperative is a form of business organization commonly used in agriculture. It differs from other forms of business in that it is owned by the users of its services or products. There is no single definition of a cooperative that encompasses all cooperatives. The University of Wisconsin Center for Cooperatives identified five factors that may be used to identify cooperatives. Not all five factors are necessarily found in all cooperatives. These factors are:

1. Statement of principles,

2. Self-identification,

3. Incorporation status,

4. Tax-filing status, and

5. Governance structure.

Cooperatives are found in all sectors of the economy including government. The University of Wisconsin Center for Cooperatives identified almost 30,000 cooperatives based upon the above factors. Together these entities held more than $3 trillion in assets, generated more $500 billion in revenue, and paid over $25 billion in wages.

The Cooperative Development Network has identified seven core principles of cooperatives. These are:

1. Voluntary and open membership,

2. Democratic member control,

3. Member economic participation,

4. Autonomy and independence,

5. Education, training, and information,

6. Cooperation among cooperatives, and

7. Concern for community.

While the above is a good general statement of cooperative principles, these principles are not universally applicable. In the discussion of marketing orders discussed in Chapter 8, it is apparent that the regulatory structure that created marketing orders has made participation in associated cooperatives less than voluntary. While producers may in theory refuse to join the associated cooperatives, that refusal may render their farming operations financially unviable. Litigation between members and some cooperatives was also discussed in Chapter 8. It is apparent that in some larger cooperatives the financial interests of management may have diverged from that of the members.

There is likely to be litigation in addition to that discussed in Chapter 8 that may render some current practices in regard to marketing orders and cooperatives unconstitutional. The increasing willingness of the Supreme Court to set aside longestablished customs has introduced additional uncertainty in some agricultural markets.

The Farm Credit institutions discussed in Chapter 5 are either borrower-owned cooperatives or cooperatives owned by constituent Farm Credit institutions. Since these cooperative institutions were created by Congress, they have been heavily regulated by the federal government, sharply limiting the traditional autonomy and independence for which cooperatives are noted. During the 1980s, when the Farm Credit system was in danger of insolvency, Congress intervened to rescue the system by closing some institutions, forcing the merger of others, and restructuring the entire system. The traditional independence of cooperatives may be limited by enabling legislation and circumstances.

TYPES OF COOPERATIVES

There are several ways to classify cooperatives. Certainly, one can use such factors as size and industry to classify cooperatives. The University of Wisconsin Center for Cooperatives uses classifications that will be used in this chapter. Those classifications are:

- Consumer cooperatives,

- Worker cooperatives,

- Producer cooperatives,

- Purchasing or shared services cooperatives, and

- Multi-stakeholder cooperatives.

Consumer cooperatives are used by consumers to purchase goods and services for their own consumption. Rural electric cooperatives that provide electricity to approximately two-thirds of the land area of the United States are an example. So is REI, a seller of camping and related recreational equipment. Worker cooperatives are owned by the employees of the company.

Producer cooperatives are owned by producers of goods or services. This chapter focusses on agricultural producer cooperatives. Ocean Spray is a large producer cooperative owned by farmers that produce for it. Purchasing or shared services cooperatives are owned by businesses rather than individuals. Multi-stakeholder cooperatives include to or more types of members.

TERMS AND PRINCIPLES

The primary purpose of private businesses is to maximize returns to the owners of capital that have invested in those businesses. That value supersedes all other values. Many have disagreed with that principle including most notably communists and socialists of various types. One solution that lies within the capitalist framework rather than rejecting that framework as communists and some socialists do is the creation of cooperatives. At various times in the history of the United States, the movement to form cooperatives have waxed and waned. Cooperatives are often seen as a way to mitigate the perceived harshness of capitalism. A cooperative is a form of nonprofit. It is distinguished from nonprofit charities in that it generally has no charitable purpose. It is designed to increase the profits of its members.

The terms used in describing cooperatives often incorporate explicitly or by implication principles of the cooperative movement. Thus, terms and principles are included in one section of this chapter. There is no universal terminology so some terms listed below will be closely related in meaning.

- Bylaws – rules not included in the articles of incorporation that specify operational practice and policy of the cooperative. For example, bylaws typically address the initiation fee for new members, annual fees if any, and the dollar amount of business that a member must do with the cooperative each year. Bylaws may usually be changed by a vote of the membership. Changes to bylaws are usually proposed by members of the board of directors; however, many cooperatives allow changes to bylaws to be proposed by any member.

- Charter (articles of incorporation) – is the document that creates the cooperative just as the document of the same name created a regular business corporation. This document must abide by the laws of the state where the cooperative was created and be filed with the state agency responsible for business entities. Usually there is a filing fee plus annual fees that must be paid. In many states those fees are lower than for regular business corporations.

- Director – members of a cooperative elect directors to oversee management of the cooperative much in the same way that stockholders elect directors to perform the same task. Typically, the directors (or the members) will select one director to serve as chair (or president) of the board of directors. The directors may also elect other officers that may include a vice-chair, a secretary, and a treasurer.

- Manager – the directors hire a person (that may be a corporate entity) to conduct the day-to-day business of the cooperative.

- Member – is a person that joins the cooperative by becoming an owner, usually through the purchase of one share of stock.

- Outside director – a director that is not a member of the cooperative. Usually outside directors do not have a vote. An exception is the Farm Credit System (discussed in Chapter 5) whose institutions are required to have outside directors with votes. Certain individuals cannot be directors if they have a substantial role in a competitor as such an arrangement is called an interlocking directorate that may violate federal antitrust laws.

- Patron – is a person that does business with a cooperative. A patron is not required to be a member. Non-member business is the term used to describe business done with the cooperative by non-member patrons.

- Patronage refund (dividend) – funds not needed to cover costs that are distributed to patrons.

- Per unit retain – retention of funds is usually based upon the total volume of business that the patron does with the cooperative. For example, if the patron sells wheat to the cooperative, the funds retained will be based upon the number of bushels sold.

- Retained patronage – There is usually a delay of several years before retained funds are paid. These funds are used as a reserve to ensure that there are sufficient funds for operating the cooperative.

- Voluntary and open membership – cooperatives are voluntary organizations with membership open to all that use the cooperative’s services. With commodities subject to marketing orders that use cooperatives (such as dairy) the economic disadvantages of not joining as such that farmers may not feel that becoming a member is voluntary.

- Democratic member contro l – cooperatives are, in theory, controlled by members. In large cooperatives, control for an individual member may be limited. There is an inherent conflict between the managers of a cooperative and its members. As discussed in Chapter 8, there has been litigation between members and the cooperative over allegations of unfair treatment.

TAXATION

Cooperatives are pass through entities. Cooperatives do not make a profit. To have tax treatment as a cooperative, the organization must subordinate capital, have democratic control by members, and allocate margins based on patronage. Cooperatives do not pay tax on patronage income. Tax is determined and paid at the member level. Farmers pay tax on patronage income only in the year that the income is received.

Properly reporting patronage income can be complex. The following example from IRS Publication 225 (the 2023 Farmer’s Tax Guide) illustrates this complexity.

Example. On July 1, 2022, Mr. Brown, a patron of a cooperative association, bought a used machine for his dairy farm business from the association for $2,900. The machine has a life of 7 years under MACRS. Mr. Brown files his return on a calendar year basis. For 2022, he claimed a depreciation deduction of $311, using the 10.71% depreciation rate from the 150% declining balance, half-year convention table (shown in Table A-14 in Appendix A of Pub. 946). On July 2, 2023, the cooperative association paid Mr. Brown a $300 cash patronage dividend for buying the machine. Mr. Brown adjusts the basis of the machine and figures his depreciation deduction for 2022 (and later years) as follows.

Cost of machine on July 1, 2022 $2,900

Minus: 2022 depreciation $311

2023 cash dividend $300 $611

Adjusted basis for

depreciation for 2023: $2,289

Depreciation rate: 1.0 ÷ 6½ (remaining recovery

period as of 1/1/2023) = (0.1538)

× 1.5 = 23.07%

Depreciation deduction for 2023

($2,289 × 0.2307) $528

From the above example, it should be apparent that most farmers doing business with cooperatives will need the assistance of tax professionals. To summarize, as a rule cooperatives do not pay income tax on patronage income that they retain. Farmers do not pay tax until the year the patronage income is actually paid to them. For cooperatives this rule gives them a tax-free source of capital. Farmers get the advantage of paying taxes only in the year that the income is received. Nonpatronage income of a cooperative is taxable to the cooperative.

Example 12.1. XYZ Farmer Cooperative keeps surplus funds in CDs with a local bank. This interest income is not patronage income because it is not derived from its income with its farmer patrons.

Some cooperatives pay no patronage refunds to patrons that are not members. The income attributable to non-member patrons that is not distributed is taxable income to the cooperative.

FORMATION

Creating a cooperative takes effort, knowledge, clear thinking, professional advice, capital, and clear thinking. USDA Rural Development Cooperative Information Report 7 (hereinafter, Report 7) lists four reasons for establishing marketing cooperatives and two reasons for establishing purchasing cooperatives to acquire goods and services.

Marketing cooperatives

- Improve bargaining power— by combining the volume of members, cooperatives leverage their position when dealing with other businesses.

- Reduce costs—volume purchasing reduces the purchase price of needed supplies. Earnings of the cooperative returned to individual members lower their net costs.

- Obtain market access—value is added to products by processing or offering larger quantities of an assured type and quality to attract more buyers.

- Improve product or service quality—when a cooperative is in a market, the quality of products or services is often improved because of enhanced competition.

Source: Report 7.

Purchasing cooperatives

- Obtain products or services otherwise unavailable— cooperatives often provide products or services where the level of demand would not likely attract private businesses.

- Reduce costs/increase income—reducing the cooperative’s operating costs through the cooperation of many members increases their earnings.

Source: Report 7.

Typically, farmer cooperatives do both purchasing and marketing so these purposes will be discussed together. For many buyers dealing with marketing cooperatives saves them money because they need to deal with one entity rather than hundreds of individual farmers. For that benefit, buyers are often willing to pay a premium because they reduce their purchasing costs and can be assured product of uniform quality.

For purchases, volume discounts that would be unavailable to individual farmers can be obtained. Some wholesalers have minimum quantities that they will sell. These minimum quantities are often too large for an individual farmer to purchase the product. Given the geographic isolation of many farmers there may be no retailer within a reasonable distance.

For farmer-owned cooperatives, there is a partial antitrust exemption discussed below. This creates substantial advantages for farmers operating through farmer-owned cooperatives.

USDA has a great deal available to help with farmer-owned cooperative creation. This assistance includes both technical expertise and financial assistance.

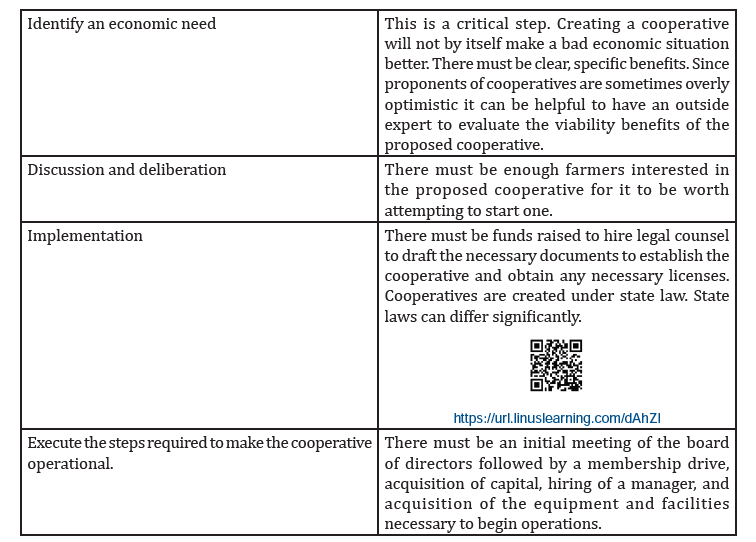

Report 7 lists twelve steps to formation of a cooperative. Table 12.1 summarizes this in abbreviated form.

Table 12.1 : Steps to forming a cooperative.

For the full twelve steps along with a useful discussion of what is involved in each step please see Report 7.

It is important for directors to take steps to ensure that their actions are in compliance with the law. Those steps should begin at the creation of the cooperatives. The 1929 edition of Legal Phases of Farmer Cooperatives stated:

“Membership on the board of directors of a cooperative is ordinarily looked upon as a post of honor, but the board member who has examined the statutes and court decisions on the subject will also look upon the office as a post of great legal responsibility. Not only does the welfare of the cooperative rest upon the board as a group, but the office of director carries with it the possibility of large personal liability both at common law and under statutes.”

That statement made almost 100 years ago continues to be accurate. All cooperatives should have a compliance officer that reports directly to the board of directors. All major actions should be reviewed by counsel prior to taking those actions. Officers’ and directors’ insurance is a necessity since officers and directors may be personally liable for their actions. Civil liability may arise from breach of fiduciary duty, and negligent, intentional, and strict liability torts. Criminal liability may arise from food safety violations, worker safety violations, other violations involving health and safety, antitrust violations, and many other violations. Liability may arise from either federal or state law. Officer and directors’ insurance does not cover criminal violations. For covered civil violations, insurance general pays the cost of defense as well as any judgment.

EQUITY ACCUMULATION

EQUITY ACCUMULATION Since returns to investors are not the highest priority for cooperatives, attracting capital is a constant problem. Congress created a system whereby the money from selling bonds is available to Farm Credit institutions. This is described in Chapter 5. Most cooperatives do not have this option.

The passthrough treatment of cooperatives helps eliminate this problem. Unlike business corporations that are taxed twice, the income of cooperatives is taxed once, at the member level. Direct investment by its members is one source of capital for cooperatives. Direct investment, however, is not a major source of cooperative capital. Retained earnings, called margins, and retained per unit income are more important sources of capital. Earnings from nonmember patrons that are not eligible for perunit distributions are a taxable source of retained earnings.

ANTITRUST

The Capper-Volstead Act of 1922 gave farmerowned cooperatives a limited exemption from antitrust laws. A cooperative must meet certain conditions to be covered by the Capper-Volstead Act.

- Membership must be limited to bona fide agricultural producers (farmers).

- Members must be limited to one vote or to dividends on membership capital of no more than 8% per year.

- A majority of the cooperative’s marketing business must be done with members of the cooperative.

- The cooperative must operate for the mutual benefit of its members.

Supply cooperatives, or marketing cooperatives that also act as supply cooperatives, may not qualify for protection under the Capper- Volstead Act; however, this issue has not been addressed by court decisions. Supply cooperatives have not faced the litigation that marketing cooperatives have faced.

Antitrust risks have been prevalent in areas that include agreements on prices and terms of sale, undue price enhancements, control of majority of the market by a cooperative (market share), mergers and acquisitions, customer and member selection, transportation, quantity limitations of product handled, and predatory pricing.

Cooperative officers and directors as well as their advisers may be personally liable for antitrust violations. Private parties may recover three times the amount of their injuries. There may also be liability under state unfair trade practices laws. Current civil suits involve potato, dairy, mushroom, and egg cooperatives.

Example 12.2. The Kumquat Cooperative was facing competition from a private company that had through adoption of new technology been able to sell kumquats at a lower price than the Cooperative. Larry, a director of the Cooperative, said at a directors meeting in a statement duly recorded in the minutes of the Cooperative, “We need to kill that company in its cradle. Let’s offer all their customers a lower price. That should slow them down.” The other directors enthusiastically agreed as was duly recorded in the minutes. If the competitor sues, it is likely to be able to subpoena the minutes and is likely to prevail. Both the cooperative and the directors will be liable.

CONCLUSION

Cooperatives can help farmers reach markets that they otherwise could not reach by making possible the sale of larger volumes in a single lot and by collectively marketing their product. The economics of a cooperative venture should be carefully considered. Simply forming a cooperative will not change economic conditions. When there are specific advantages that can be identified, a cooperative is much more likely to succeed.

References

AGRiP [Association of Governmental Risk Pools]. (2022). Foundational Pooling Knowledge. https://www.agrip.org/education/poolingbasics398

Carson, M. and Frederick, D.A. (2013, January/February). Antitrust challenges facing farmers and their cooperatives. Rural Cooperatives, USDA Rural Development. https://www. rd.usda.gov/sites/default/files/rdCoopMag- Jan-Feb2013.pdf

Deller, S., Hoyt, A., Hueth, B., and Sundaram-Stukel, R. (2009, June 19). Research on the Economic Impact of Cooperatives. University of Wisconsin Center for Cooperatives. https://reic. uwcc.wisc.edu/

Fee, D., Hoberg, A.C. and McCormick, L.G. (1984, December). Director Liability in Agricultural Cooperatives. USDA Rural Development, Cooperative Information Report 34. https:// www.rd.usda.gov/sites/default/files/cir34. pdf

Frederick, D.A. (2011, August 13). Managing Cooperative Antitrust Risk. USDA Rural Development, Cooperative Information Report 38. https://www.rd.usda.gov/sites/default/ files/cir38.pdf

Frederick, D.A. (2012, November 23). Antitrust Status of Farmer Cooperatives: The Story of the Capper- Volstead Act. USDA Rural Development, Cooperative Information Report 59. https://www. rd.usda.gov/sites/default/files/CIR59.pdf

Frederick, D.A. [repub. by Smith, S. M. and Chesnick, D.]. (2013, June). Income Tax Treatment of Cooperatives: Background, 2013 Edition. USDA Rural Development, Cooperative Information Report 59. https://www.rd.usda.gov/files/cir44-1.pdf

IRS. (2023). Publication 225 (2023), Farmer’s Tax Guide. https://www.irs.gov/publications/p225

Keystone Development Center (KDC). (n.d.). Developing a Strong and Equitable Cooperative Ecosystem throughout the Mid-Atlantic Region Since 1999. https://www.kdc.coop/

KDC. (2021). Stories from Our Members. https://cooperationworks. coop/resource-library/videos/ National Agricultural Law Center Staff. (2022, May). Formation of Agricultural Cooperatives. The National Agricultural Law Center. https://nationalaglawcenter.org/state-compilations/ ag-coops/

National Counsel of Farmer Cooperatives. (2023, December). Capper-Volstead Act. https:// ncfc.org/resource/capper-volstead-act/

The Cooperative Development Network. (2021). Cooperative Principles. Cooperation Works! https://cooperationworks.coop/about/ cooperative-principles/

The National Agricultural Law Center. (n.d.). Cooperatives – An Overview. https://nationalaglawcenter. org/overview/cooperatives/

USDA Rural Development. (n.d.). Cooperative Services. https://www.rd.usda.gov/programsservices/ all-programs/cooperative-services

USDA Rural Development. (n.d.). Interagency Working Group on Cooperative Development. https://www.rd.usda.gov/about-rd/initiatives/ interagency-working-group-cooperative- development

USDA Rural Development. (n.d.). Partners in Cooperative Development. https://www.rd.usda. gov/about-rd/initiatives/interagency-working- group-cooperative-development/partners

Wadsworth, J.J. and Bau, M. (2015, March). How to Start a Cooperative. Cooperative Information Report 7, 2015 revision, USDA Rural Development. https://www.rd.usda.gov/ sites/default/files/publications/CIR_7_HowtoStartaCooperative. pdf