Chapter 14: Hedging Using Agricultural Futures Markets

Hedging Using Agricultural Futures Markets

Grain marketing is an endeavor that takes real thought, preparation, planning, confidence and perhaps a little imagination.

Sean K. Treasure

Marketing agricultural commodities is inherently risky. Price risk is one of the key risks that farmers face. Farmers begin the production process months (even years in the case of tree crops) before they know the price that they will receive for their products. Discussed in this chapter are agricultural futures as a tool for managing price risk. Chapter 15 discusses agricultural options as a tool for managing price risk. Related to this topic are crop insurance, discussed in Chapter 6, Federal farm programs, discussed in Chapter 7, and marketing orders, discussed in Chapter 8.

For farmers that rent production land, some leases contain clauses that adjust rent payment for changes in commodity prices. This is another way that farmers can protect themselves from price risk. When prices drop the rent is reduced. The flip side of this is that when commodity prices rise the amount of rent paid increases. This type of lease is a form of price risk sharing between the farmer and the landlord. There is a second type of lease, the share lease, that involves even greater risk sharing by the landlord. In this type of lease the landlord provides some of the inputs in addition to the land. In return the landlord receives a share of the crop. Neither of these types of lease prevent the farmer from using agricultural futures to reduce price risk.

Figure 14.1 : Types of Futures contract https://www.financestrategists.com/wealth-management/alternative-investment/futures/

WHAT IS A FUTURES CONTRACT?

An agricultural futures contract is a type of derivative. A derivative is an asset whose value is derived from the value of some underlying asset. The underlying asset for an agricultural futures contract is the physical agricultural commodity.

This video explains what a futures contract is and contrasts it to a forward contract.

Agricultural futures contracts were developed after the U.S. Civil War to satisfy the needs of a growing agricultural industry to manage commodity price risks. Futures contracts were the first modern derivative. They offer an alternative to the spot (cash price) and forward contracts that were discussed in Chapter 13. The grading system for agricultural commodities that was discussed in Chapter 9 has been essential to the development of modern agricultural futures markets. Grades give buyers a reliable and measurable way to know that they were getting what they paid for. Where grades can be usefully applied, they are used to specify what is being traded under a futures contract. A futures contract provides certainty as to quality, quantity, time of physical delivery, and the location of delivery.

Futures Market Explained

The CME Group offers a trading simulator at no charge.

Example 14.1. Each CME Group futures contract for corn is for 5,000 bushels. The contract price is for #2 Yellow Corn. There is a premium of 1.5 cents per bushel for #1 Yellow and a discount of 2 to 4 cents per bushel for #3 Yellow. The discount on #3 Yellow is adjusted for broken kernels and foreign material and damage grade factors. Nine-month contracts are offered for delivery in March, May, or September. Eight-month contracts are offered for delivery in July and December. Delivery is done through either a warehouse receipt or a shipping certificate. Warehouse receipts must be from a CME Group approved warehouse.

Example 14.2. For live cattle futures, the unit per futures contract is 40,000 pounds. Prices are quoted as cents per pound. The meat and yield grades discussed in Chapter 9 are not used in live cattle futures contract specifications because they can only be established after slaughter. As you might guess, the delivery process for live cattle is somewhat different than for grains and oil seeds.

CME Group factsheet and video: Understanding The Grain Delivery Process https://www.cmegroup.com/education/courses/ introduction-to-agriculture/grains-oilseeds/understandingthe- grain-delivery-process.html

Please click to view the full contract specs for live cattle futures. https://www.cmegroup.com/markets/agriculture/livestock/ live-cattle.contractSpecs.html

A futures contract is a standardized contract that is traded on an exchange. These contracts are standardized as to delivery date, delivery location, and the quantity and quality of the commodity. Futures contracts differ from the forward contracts described in Chapter 13 in several important regards. Forward contracts are subject to performance risk, i.e., either the farmer or the elevator may refuse or be unable to perform their side of the contract.

Example 14.3. The Integrity Elevator Company owned 41 elevators in three states. It entered hundreds of forward contracts in 2024 for delivery to its various elevators at harvest in 2025. Integrity elevators are licensed under the United States Warehouse Act (USWA) to issue electronic warehouse receipts that are used to guarantee delivery on futures contracts and as collateral for financing. In January 2025, inspectors from USDA discovered that Integrity had insufficient wheat to cover its issued warehouse. (It had less than a third of the grain needed to cover the outstanding warehouse receipts.) Integrity’s owner, Honest Abe, disappeared, along with the money, before Federal Marshals could serve him with an arrest warrant. Integrity’s major creditors joined to file an involuntary bankruptcy petition against Integrity. Upon motion by the attorney representing the major creditors, the bankruptcy judge set aside all existing forward contracts. The farmers that had forward contracts with Integrity suddenly found themselves without the price protection that they had expected.

The risk that one party will not perform (as illustrated in Example 14.3) is known as counterparty risk. Futured contracts eliminate counterparty risks. The exchange which is highly regulated buys from the seller and sells to the buyer. The exchange assumes the risk that either the seller or the buyer does not perform. Exchanges such as those owned by the CME Group are private businesses. They are regulated by the Commodity Futures Trading Commission (CFTC), an agency of the Federal government.

What is the Commodity Futures Trading Commission CFTC

This CME Group video explains how CME Clearing operates to ensure integrity in settling trades and in eliminating counterparty risk.

The CFTC regulates every aspect of trading futures and options. The regulations are designed to ensure that buyers and sellers and clearing houses have financial depth sufficient to eliminate counterparty risk. An additional advantage of exchange traded futures markets is that they have depth. Depth means that there are many participants in the market. If one wants to either buy or sell there is almost always a counterparty available. Events under which the market is illiquid are extremely rare. Exchanges have certain circuit breakers built in. If the market falls or rises above a certain percentage amount, trading will be temporarily halted. Each exchange establishes its own rules for setting price limits and determining the amount of time that trading is halted.

CME Group Grain and Oilseed Price Limit FAQ

Futures contracts allow the parties to the transaction to be anonymous because only the exchange knows the identity of both the buyer and seller. Unlike forward contracts, futures contracts are liquid. If a seller or buyer of a futures contract wishes to close their position prior to the delivery date it is a simple matter of buying the opposite contract thereby extinguishing both contracts. Forward contracts are not easily transferred to another party. Delivery is generally expected.

There exist futures contracts that are not exchange traded. These are traded in the over the counter (OTC) market. Trades occur with little or no intermediation. Unlike exchange traded futures both the buyer and seller have counterparty risk. Contracts are not standardized. The over-thecounter market is typically thin, which makes the market illiquid. A thin market is one that has few traders. In terms of risk profile, the OTC contracts are similar in risk to forward contracts. They may be riskier because the farmer has usually done business with the elevator offering the forward contract for many years. A farmer entering an OTC contract seldom knows anything about the counterparty to an OTC contract.

Over-The-Counter (OTC) Trading and Broker-Dealers Explained in One Minute: OTC Link, OTCBB, etc.

The major exchanges offer OTC futures as a service to their customs. Unlike regulated futures contracts, the exchanges do not guarantee performance. Exchanges that offer OTC futures contracts never take ownership of those contracts. The exchange is a broker only. Unlike regulated futures contracts, the exchange never takes ownership of OTC futures.

What is the value of using futures contracts?

Farmers and users of agricultural commodities rely upon futures contracts to manage their price risk through hedging. A hedge has two parts which, taken together, cancel each other. In this chapter we will explore how such an arrangement can be used as a tool to manage price risk.

Futures markets have other important uses. Providing information about the pricing of agricultural commodities is one of the most important. Economists call this “price discovery.” Grain elevators use information from the futures markets in setting the cash prices that they offer, and the prices offered on their own forward contracts. Buyers at livestock auctions use future market prices to help determine their maximum bids.

Futures serve as the underlying asset for option contracts that will be discussed in Chapter 15. Without futures contracts, options markets as they operate today could not exist.

Figure 14.2 : Farmers and users of agricultural commodities rely upon futures contracts to manage their price risk through hedging among other strategies. https://www.financestrategists.com/wealth-management/investment-risk/market-risk/

Definitions

Arbitrage – the practice of making money by trading on two or more exchanges to profit from price differences between exchanges for the same commodity. Arbitrageurs play a critical role by ensuring that prices for the same commodity do not substantially diverge in different markets.

For a comprehensive glossary see the CME Group glossary. It includes options terms that will be discussed in Chapter 15.

Basis – Premiums were mentioned briefly in Chapter 13. Another name for premiums is basis. A futures price is national. Basis is highly local. Basis reflects transportation costs to major domestic users or export ports. There are other factors that go into basis. These factors include local shortages or surpluses, quality, differences in time periods, and the number of competitors in a local market. Most elevators adjust the basis that they apply about twice a day unlike futures prices that change constantly. Basis is calculated as the difference between the futures price and the local cash (spot) price.

Farmers must know the basis that will be applied to their product in addition to the futures price if they are to know what they will net from selling their product. It is good practice for farmers to keep a spread sheet of historical basis levels in their marketing area. The USDA Agricultural Marketing Service through its Market News provides some national and regional basis information. This is a good starting point. Some farmers are fortunate enough to farm in areas where their local Land Grant university collects and publishes this information.

Kansas State University Interactive Crop Basis Tool

Basis risk – the risk that the basis will widen or narrow over the life of a hedge position. Under normal market conditions the basis can be expected to narrow (converge) as the expiration of a futures contract approaches. There is never a guarantee that market conditions will be normal.

Clearing house – the organization within an exchange that ensures that buyers and sellers can conduct their trades without counterparty and other risks. A clearing house conducts risk monitoring 24 hours a day, six days a week. It does daily markto- market which is the process by which the value of an asset is adjusted for market conditions. This activity is essential to ensure that adequate margins are maintained by all traders. The clearing house recalculates performance bond requirements daily.

CME Group: Clearing House Risk Management

Cost of carry (sometimes just carry) – the cost of storing a physical commodity. It includes the cost of storage, insurance, and finance charges.

Crop reports – reports prepared by USDA about crop conditions. Understanding these is critical to successful participation in futures and options markets.

Please look at the various reports that USDA prepares.

Daily trading limit – the maximum amount of price variation allowed in one trading day. Trading may be stopped if the limit is exceeded. The purpose of limits is to promote market stability.

Delivery – the point at which title to the physical commodity changes from the seller to the buyer.

Expiration – the last trading day for a futures contract.

First Notice Day – the day upon which sellers of futures contracts are notified of their obligations to deliver physical commodity to buyers, It is also the point in time at which sellers and buyers are matched.

Livestock reports – reports prepared by USDA about livestock and poultry supply and market conditions.

View reports that AMS prepares on livestock and poultry as well as crops.

Long – farmers are inherently long because they have or will have at harvest, the physical commodity. Long positions have no corresponding short positions.

Maintenance Performance Bond – the minimum amount of equity that a market participant must maintain to prevent the exchange from closing the position. This is more commonly called margin. When the equity in the customer account falls below the minimum level, the exchange makes a margin call, a demand to add money to the account.

Market maker – a firm or person with trading privileges that is contractually obliged to buy when there is an excess of contracts offered or sell when there exists an excess of contracts desired. Market makers play a critical role by maintaining market liquidity. Without market makers there would be times when buyers could not buy, or sellers could not sell. Market makers are private businesses that hope to make money on the spread between what they pay for contracts and what they sell them for. Market makers need deep pockets because there are times when they lose money. Usually, market makers specialize in only a few contracts.

Mark-to-market – At the close of the market day, all contracts in market participants’ accounts are valued at the closing price. Those that no longer have the minimum equity in their accounts are issued margin calls. The exchange will liquidate the accounts of any market participants that fail to restore the equity in their accounts.

Maturity – the period during which the futures contract can be settled by actual delivery. The period runs from the first notice day to the last trading day for the futures contract. If the holder of the futures contract wishes to close the position prior to delivery, a corresponding contract must be purchased no later than the last trading day of the contract.

Offset – closing an open position by buying the opposite contract or by making or taking delivery.

Offsetting (lifting) a hedge – the means of closing a futures hedge. Discussed in detail in the section in this chapter on hedging.

Short – users of commodities (such as flour and feed mills) that need to buy the commodity. Short positions have no corresponding long positions.

Underlying (asset) – the asset upon which the value of a derivative is based. Physical agricultural commodities are the underlying for agricultural futures. The underlying for agricultural options are agricultural futures.

Volatility – the change in price over time.

Mechanics of futures contracts

Futures contracts are three party contracts. There is the seller of the contract. There is a buyer of the contract. The third party is the exchange clearing house which buys from the seller and sells to the buyer. It is this aspect of futures contracts that ensures that contractual and financial obligations are met. The exchange sets the rules for buyers and sellers including the level of risk that buyers and sellers are allowed to take. Both buyers and sellers are required to have sufficient financial capacity such that they are likely to fulfill their contractual obligations.

Futures contracts require sellers to deliver and buyers to take possession of physical agricultural commodities. Since most futures contracts are closed prior to the delivery date, market participants sometimes lose sight of the fact that these contracts are about physical commodities.

To work with futures contracts, one must understand the codes used to identify each contract. These can be found on each exchange’s website. Different exchanges sometimes use different codes for the same contracts. The CME Group uses the following month codes.

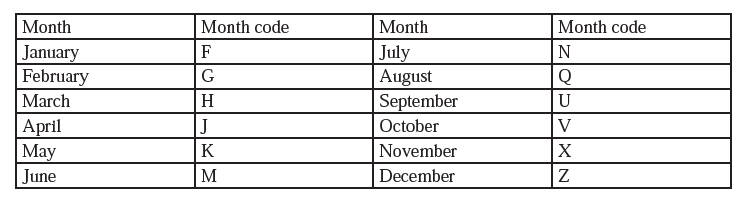

Understanding contract trading codes

Codes are three or four letters. The first one or two designate the commodity, the third is the month code, and the fourth is the year. For example, ZCZ4 is the code for corn for December 2024 delivery.

Delivery is not available in every month of the year for most commodities. Corn contracts are available for delivery in the months of March, May, July, September and December.

A futures contract is completed by delivery of the physical commodity by the delivery date at a specific delivery point. All contracts are standardized. Most grain and oilseed contracts are for 5,000 bushels. These contracts are traded in quarter cent increments. Trading is done through licensed brokers that are approved by the exchange. Brokers charge a commission to those trading. The commission is in addition to the price of the futures contracts.

Table 14.1 : Month Codes

Those opening a brokerage account are not expected to put up the entire value of the expected trades. An initial margin is required to be deposited with the exchange. The value of futures contracts in each account is marked-to-market at the daily close of trading. Every account that has lost money is expected to be replenished by depositing a maintenance margin with the broker.

Participants in futures markets

There are three types of participants in futures markets. They are hedgers, speculators (traders) and arbitrageurs.

Hedgers take neutral positions that are intended to lock in an acceptable price. Hedgers are inherently short or inherently long. A feed mill that makes cattle feed is inherently short. It buys grain to use in making feed. A farmer that grows grain is inherently long because the farmer produces grain and needs to sell it. Hedging is discussed in detail below.

Speculators, also called traders, make their money by trading futures and options contracts. Speculators have no interest in the underlying physical commodity (beyond the knowledge needed to trade futures and options for which the commodity is the underlying). Speculators never take delivery on a futures contract. They are generally not equipped to handle physical commodities.

Figure 14.3 : Participants in futures markets

In times of rising food prices such as the current time, politicians often accuse the food industry of ‘price gouging’. In the four years that have elapsed since July 2019, retail grocery prices have risen overall by 27%. In such times speculators are sometimes singled out for demonization by politicians. Speculators do at times make outsized profits, however, there are times when they have outsized losses. Their losses get less press coverage than their profits. Speculators are the group that collectively absorb the risk that hedgers are paying to avoid. Some of the positions that they take expose them to high risks of loss (but also high potential gains).

Despite the scorn that speculators sometimes receive they are essential to well-functioning markets. They provide liquidity that ensures that contracts are (almost) always available when hedgers wish to buy them. By providing the single largest group of the three group of market participants, speculators provide the market with depth that improves price discovery. Thin markets (few participants) are notorious for poor price discovery. Most speculators specialize in a few commodities. They are likely to understand them much better than the typical hedger that spends most of their time growing wheat or milling flour or some other activity. The collective knowledge of speculators in a commodity is embodied in the prices of futures contracts for that commodity.

The third group are arbitrageurs. Arbitrage is the practice of trading in two or more markets with the objective of profiting from differences in prices for the same commodity in different markets. With most markets being electronic it is now common for arbitrageurs to practice their trade globally. This activity prevents prices from diverging irrationally. Divergent pricing is an indication that markets are not functioning efficiently.

Hedging

A hedge is a position whereby changes in prices do not affect the amount the hedger makes (or pays). There are two types of hedges using futures, selling hedges and buying hedges.

A selling hedge is used by producers of a commodity to manage their price risk. Farmers are sellers that could benefit from a selling hedge. The position of a farmer is inherently long because farmers produce and have the physical commodity, e.g., corn grain. The futures contract that a farmer sells is a short contract because at delivery the farmer will be required to come up with the physical commodity. Unless the farmer already has grain in the bin from a prior crop year, it is best to contract for no more than 40% of the expected crop. If the farmer’s crop is less than the contract amount the farmer will need to either close the futures contract at a loss or go into the market and buy physical commodity to deliver.

This Kansas State publication provides additional detail and examples of the selling hedge.

A buying hedge is used by purchasers of inputs to manage price risk. A feed manufacturer uses grains as an input. It could benefit from a buying hedge. A livestock feed lot that does its own feed manufacturing is both. It can manage price risks associated with the commodities it buys to use in

This Kansas State publication provides additional detail and examples of the buying hedge.

References

CFTC. (2024). About the CFTC. https://www.cftc. gov/About/index.htm

CME Group. (2024, July 11). Agricultural futures and options. https://www.cmegroup.com/ markets/agriculture.html#overview

Dodd, R. (2008, June 1). Over-the-Counter Markets: What Are They?. F&D Magazine. International Monetary Fund. https://www.imf.org/external/ pubs/ft/fandd/2008/06/basics.htm Futures Fundamentals. (n.d.). About

Futures Fundamentals. https://www.futuresfundamentals. org/about-futures-fundamentals/

Mintert, J., Waller, M. and Borchart, R. (1999, January 1). Introduction to Futures Markets. AgManager, Kansas State University. https:// www.agmanager.info/livestock-meat/marketing- extension-bulletins/price-risk/introduction- futures-markets

Newman, J. and Nassauer, S. (2024, August 20). Food Industry Pushes Back Against Kamala Harris’s ‘Price Gouging’ Plan. The Wall Street Journal. https://www.wsj.com/politics/ policy/food-industry-pushes-back-againstkamala-harriss-price-gouging-plan-064c3b b1?st=zkwymsqfzyna1cb&reflink=desktop webshare_permalink

Robe, M.A. and Roberts, J.S. (2019, June). Who Holds Positions in Agricultural Futures Markets —and How? CFTC. https://www.cftc.gov/ node/215786

Sartewelle III, J.D., Smith, E., Kastens, T., and O’Brien, D. (1998, November). Buying Hedge with Futures. AgManager, Kansas State University. https://www.agmanager.info/ grain-marketing/interactive-crop-basis-tool/ buying-hedge-futures

Sartewelle III, J.D., Smith, E., O’Brien, D. and (1998, November). Selling Hedge with Futures. AgManager, Kansas State University. https://www.agmanager.info/grain-marketing/ interactive-crop-basis-tool/sellinghedge- futures

Treasure, S.K. (2015). The Farmer’s Guide to Grain Marketing: Maximizing Profit While Minimizing Risk.

USDA AMS. (2024). USDA Market News. https:// www.ams.usda.gov/market-news