Chapter 06: Insurance

Insurance

There are known knowns. These are things we know that we know. There are known unknowns. That is to say, there are things that we know we don’t know. But there are also unknown unknowns. There are things we don’t know we don’t know.

Donald Rumsfeld

WHAT IS INSURANCE?

Insurance is a contractual relationship that involves the transfer of risk from one party to another. A risk is a loss to which a probability distribution can be assigned. A probability distribution allows accurate prediction of the loss likely to be experienced by a large group of similarly situated insureds. An insured is the one that purchases a policy under which the insurer (the insurance company) agrees to assume some of the insured’s risk of loss. The insured pays a premium to the insurance company to compensate it for assuming the covered risk.

Figure 6.1 : Insurance is a contractual relationship that involves the transfer of risk from one party to another.

Example 6.1. Herman and Hermina, husband and wife, realized that neither could afford their house without the other’s income. To protect themselves in the event of the death of one, they decided to purchase reciprocal life insurance policies. Herman and Hermina are both 40 years of age and in good health. Herman was shocked to discover that his premium was significantly higher than Hermina’s. Outraged at this blatant gender discrimination, Herman protested to his insurance agent. His insurance agent explained that Herman posed a higher risk of loss to the insurance company than Hermina. A 40-year-old White male will live, on average, an additional 36.8 years whereas a 40-year-old White female can be expected to live an additional 41.1 years.1

How insurance works.

For an insurance contract to be enforceable, there must be a potential financial loss that the insured is insuring against. Herman and Hermina would each incur a financial loss if the other died. Herman could not buy a policy a life insurance policy on an unrelated person whose death would not cause him a financial loss. A contract that does not involve a financial loss if the covered event occurs is a gambling contract, not an insurance contract. The distinction is important because insurance and gambling contracts are regulated quite differently. Many states ban or severely restrict the subject matter of gambling contracts. Contracts on the life of another that is unrelated to the person buying the contract are generally prohibited as inducements to murder.

Insurance is fraught with the danger of moral hazard. Moral hazard is the likelihood that the existence of the insurance contract will encourage riskier behavior or even fraud. Example 6.2 illustrates an extreme, but hardly unknown, example of moral hazard.

Example 6.2. Two elderly gentlemen were lounging on chairs overlooking Miami Beach. One was from the East and the other from Kansas. The man from Kansas spoke first, “What do you do for a living?” The man from Chicago replied, “I am retired. I owned a shop in the East. It burned to the ground. Rather than rebuild I took the insurance check and retired.” The man from Kansas replied, “I have a similar story. I owned a gas station in Kansas that was leveled by a tornado. At my age, it made sense to take the insurance check and retire.” A long silence followed. Finally, the man from the East spoke, “My curiosity is getting the better of my judgment. I am truly puzzled. How did you start a tornado?”

INSURANCE TERMINOLOGY

Insurance has its own language that one must know in order navigate the complicated world of insurance. What follows is an explanation of some of the terms that everyone buying insurance for a farm or business should know. While much of the terminology is the same from one state to another, definitions of some terms vary from one state to another. Each state regulatory agency is its own lexicographer. One must look to the glossary of terms provided by most state regulators to determine the meaning of terms used in a particular state.

Actuary

An actuary is the professional that determines the cost of risk. The cost of risk is the key factor that the underwriter uses to set the premium for a particular policy. Actuaries have intensive training in the science of statistics and prepare actuarial tables from which the cost of risks can be determined. Life tables that are created from data collected by the Center for Disease Control and Prevention (CDC) are an example of an actuarial table.

Additional insured (third-party beneficiary)

An additional insured is a person that is insured by the policy in addition to the policyholder.

Figure 6.2 : An additional insured is a person that is insured by the policy in addition to the policyholder.

Adjuster

An adjuster is the professional that adjusts the claim. The adjuster will make an initial determination that the loss is covered by the policy. Once the adjuster determines that the loss is covered, the adjuster will determine the amount of the loss. It is often the case that part of the loss will be covered and part will not be covered. If the insured is not satisfied with the amount offered most insurance companies provide the opportunity to appeal to a higher level in the company. Adjusters may be in-house employees of the insurance company or may be independent contractors of the insurance company.

Admitted Carrier

An admitted carrier is an insurance company that is authorized to do business in the state where it is writing policies. Clients of admitted carriers are protected from insolvency of their carrier by state guaranty or solvency funds.

Agent/Broker

A broker is an independent business that helps the client find the insurance company that will write the needed coverage. A broker can sell policies written by any admitted carrier with which the broker has a contract to sell policies. An agent is an employee of the insurance company that writes the policy and is usually restricted to selling policies only for that company. Sometimes brokers are called independent agents. Agents that are employees of a single insurance carrier (company) are sometimes called captive agents. This brief discussion does not cover all the arrangements that exist, e.g., many captive agents are independent businesses rather than employees. Both brokers and agents are licensed by the state insurance agency that regulates insurance in the state where they sell policies.

Business interruption

An event such as the disruption caused by a storm or a strike against a major customer. Many business interruptions are insurable events.

Captive insurance companies

A captive insurance company is an insurance company that is owned or controlled by the entity that it insures. There are various cost and coverage advantages to businesses that have a captive carrier. This is an option only for entities with sufficient expertise and financial depth to set up or purchase a captive.

Certificate of insurance

Proof that an insurance company issues to a third party with an interest in ensuring that an insured has coverage. For example, a commercial landlord might require a tenant to carry liability coverage. The certificate of insurance provides proof and the key terms of such coverage.

Claim

An event gives rise to a claim. Once an event occurs that creates a loss, the insured must generally make a claim to the insurance company for payment. Claims generally require adjustment before being paid.

Deductible

The amount that the policyholder pays before the insurance policy pays. In general, the higher the deductible, the lower the premium.

Duty to defend (defense coverage)

The contractual obligation of an insurance company to pay for the legal defense, including attorney and expert fees, incurred in the legal defense of an insured.

Earthquake coverage

Earthquake coverage covers damage to both real property and personal property as the result of an earthquake.

Earthquake coverage

Endorsement (rider)

Often the standard contract that an insurance company provides will not provide adequate coverage to meet the client’s needs. In such a case, the insurance company may provide an endorsement to provide the additional coverage. An additional premium will be required for the endorsement.

Environmental impairment liability (EIL) coverage

EIL coverage provides the insured for protection in the event of a negligent act or omission that results in environmental contamination that requires remediation.

Environmental pollution liability (EPL) coverage

EPL coverage provides the insured protection from claims for personal injury or property damage arising from environmental contamination.

Errors and omissions coverage

Coverage carried by professionals such as engineers to cover any damages caused by their unintentional acts or omissions that lead to damage to their clients. It is like malpractice insurance carried by attorneys and physicians.

Excess liability insurance

Excess liability insurance provides coverage above that provided by the primary policy.

Exclusions

Risks that are not covered by a policy.

Flood insurance

Flood insurance covers flood damage. Policies are sold by private insurance companies; however, the rates are set and subsidized by the Federal government under the National Flood Insurance Program.2 It provides coverage for residences and commercial structures. It does not provide coverage for growing crops. That coverage is provided through the Federal crop insurance program, discussed elsewhere in this chapter. The Coastal Barrier Resources Act (CBRA) of 19823 prohibits Federal flood insurance in certain coast areas including the Great Lakes. Private, unsubsidized flood insurance is available in these areas. It is known as CBRA coverage.

Flood insurance

Insurable interest

An insurable interest is anything for which an insurance company can write policy. It must be something, the loss of which gives rise to a financial loss on the part of the insured. Many interests are insurable. These include damage to property, loss of business income, and liability to others for negligent injuries that one causes. Some interests are not insurable. These include liability arising from criminal acts and intentional torts. The concept of an insurable interest is complex and will be discussed in more detail later in this chapter.

Loss ratio (sometimes, relative loss ratio)

Calculated by dividing an insured’s claims by the amount of premiums paid during a period. It is an indicator of the effectiveness of the insured’s loss prevention efforts. Since it provides a numerical way of comparing similarly situated insureds, it can be used in calculating future premiums.

Negligence

Negligence is the failure to exercise reasonable care. Damages arising from negligence are generally covered by most liability policies.

Policy

An insurance policy is a contract between two or more parties. The party transferring the risk is known as the insured, and the party providing the coverage is the insurance company or insurer. The policyholder is the owner of the policy and is usually, but not always, the insured. The four corners of the policy determine what risks have been covered. Any oral statements made by an agent or broker are irrelevant to coverage, except where the terms of the policy are ambiguous. (See Example 6.6)

Policy limit

The maximum amount that the policy will pay.

State guaranty or solvency funds

State guaranty or solvency funds are created by states to protect policyholders from the insolvency of the insurance company that wrote their policy. Usually, these funds provide only partial protection from losses incurred in insurance company insolvencies.

Premium

The premium is the payment that the policyholder makes to the insurance company for providing coverage. Coverage includes all those risks that the insurance company has agreed to pay should an event occur. An event is something, e.g., a flood or a tornado, that creates a covered loss on the part of the insured. Most premium payments are periodic, typically annual. Some premium payments may be one-time as is the case with title insurance and some life insurance.

Products liability

Liability associated with products grown, produced, etc. A special products liability body of law applies to claims arising from defective products.

Punitive damages

Damages associated with intentional acts or acts that are grossly negligent. These damages are in excess of economic damages and are designed to punish. Many insurance policies exclude payment of these damages, particularly where the acts giving rise to damages were intentional. Ther is a major exception for news media defamation coverage. Defamation is, by definition, the result of an intentional act.

Reinsurer

A reinsurer arranges coverage for the risks that insurance companies have taken on.4 It is paid by the insurance company for doing so. If the insurance company receives no claims, the reinsurer keeps the money it was paid to take on the risk. If there are claims the reinsurer reimburses the insurance company for the claims that it paid.

A reinsurer may hold the risk itself or transfer the risk to investors. If there are no claims the investors make money. If there are claims, the investors reimburse the reinsurer for the money that the reinsurer paid to the insurance company. The money the reinsurer pays to the insurance company reimburses it for claims that it has paid on policies that it sold.

The insurance business is a global business. Lloyds of London is the oldest reinsurance market in the world. Without this global network of companies, U.S. insurance companies would soon exhaust their reserves and be unable to issue new policies.

Self-insurance

Use of a company’s own resources to fund its losses.

Subrogation

The right of an insurance company to seek recovery of money paid to an insured from a third party that caused the loss.

Surplus lines insurers

Sometimes no admitted carrier writes the policy that a client needs. Licensed brokers are authorized to find the surplus lines insurance that meets the needs of their clients. Surplus lines insurers are not licensed in the state where the policy is sold; however, surplus lines insurers must meet certain minimum reserve and other requirements before they can sell surplus lines insurance. Surplus lines insurers may be either foreign, i.e., licensed in another state, or alien, i.e., licensed in a foreign country. They do not participate in state guaranty or solvency funds. Policyholders have no protection in the event of the insolvency of a surplus lines insurer.

Title insurance

Title insurance covers defects in real estate titles. In is usually purchased at the time of real estate closings.

Title insurance

Umbrella liability insurance

Excess liability insurance that provides excess coverage for several primary policies, e.g., general farm liability policy and motor vehicle policies. Umbrella liability insurance also covers unknown risks, i.e., unknown unknowns.

Figure 6.3 : Umbrella liability insurance

Underwriter

The underwriter is the employee of the insurance company that determines whether a policy will be written and under what terms. Agents and brokers are not authorized to write insurance policies.

Regulation of insurance companies

The regulation of insurance companies is primarily at the state level. The most important exception to this rule is for Federal crop insurance that is regulated jointly by the Federal and state governments. Federal crop insurance is discussed in a separate section of this chapter.

To issue policies in a state, an insurance company must be an admitted carrier. Admitted carriers are subject to the full regulatory authority of the state (or states) in which they operate. Regulations cover virtually every aspect of operating an insurance company. Such matters include reserve requirements, policy provisions, and prohibited practices. Most insurance companies as well as banks and credit unions are prohibited from filing for bankruptcy.5 State laws have created insolvency proceedings under the authority of which insurance companies that cannot pay claims are put into receivership.1 Most states have guaranty or solvency funds that are used to compensate insureds of companies put into receivership. Typically, the recovery for an insured is only part of what was owed.

1. A receivership is an entity that holds the assets of an insolvent company until a receiver (usually appointed by a court) can use those assets to pay policy holders and other creditors.

Some states support (subsidize) insurers of last resort for those that cannot obtain insurance from any other source. It is restricted to certain lines, primarily home insurance.

Agents, brokers, and adjusters must be licensed in the state or states in which they sell insurance or operate. There are typically different categories of licenses.

Companies that are not admitted carriers may sell insurance in a state under limited circumstances where the insurance cannot be provided by an admitted carrier. These companies are called surplus lines insurers. They are not licensed in the state nor are they subject to the state’s supervision. These companies must meet certain reserve and other requirements. Surplus lines insurers do not participate in guarantee or insolvency funds. Insureds are unprotected in the event of a surplus lines insurer insolvency.

TYPES OF INSURANCE COMPANIES

Insurance companies may be either stock companies or mutual companies. Mutual insurance companies are owned by the insured. Any excess premiums collected are eventually returned to the insureds. Funds may be held for several years as reserves until it is determined that they are not needed. Stock companies are investor-owned companies that pay dividends to stockholders based upon the company’s profits.

While one might expect that a mutual insurance company would have a cost advantage, there is very little observed difference between the two types of companies. The level of competition in the insurance industry results in premiums that are competitive in both types of companies.

There is also an entity called a risk pool that provides a service like insurance. The idea is that a group of similarly situated entities pool their financial resources to provide risk mitigation. Risk pools have been used most successfully by associations of governments such as counties. Attempts have been made to use such pools by certain agricultural producers whose operation have difficulty finding insurance. These pools have tended to fail for lack of financial depth.

Example 6.3. Agritourism operations do not always have an easy time obtaining liability coverage. A group of agritourism operators decided to form a risk pool as an alternative to traditional insurance. Everything went well until they had their first claim. One of the operators failed to mow the grass in his parking area. The high grass was set on fire when it came in contact with a catalytic converter. Twenty-five cars were deemed total losses as the result of the fire. The average value of each car was $40,000, for a total loss of 1 million dollars. There was insufficient money in the fund to fully cover all of the claims.

Insurance needs

General farm liability insurance is the basic insurance carried by most farms. It is designed to cover legal liability arising from accidents on a farm that injure third parties. It also protects farm owners from lawsuits arising from injuries to trespassers and those on the land with permission (invitees and licensees). Most general farm liability policies include some products liability insurance. That coverage is generally limited to liability arising from raw agricultural commodities. The typical farm insurance policy also includes some property/casualty coverage. The typical farm policy does not include on-road motor vehicles, growing crops or livestock, stored agricultural commodities. Coverage for these risks must generally be purchased separately.

For larger farming operations the policy limits of the products liability coverage provided in the typical general farm liability policy are generally insufficient. For those farms that do some processing, the products liability coverage provided in the typical general farm liability policy usually excludes value added product. The language of each policy determines the dividing line between raw agricultural products and value-added products is determined by the policy language. Any doubts about whether a product is a raw agricultural commodity or a valueadded product should be resolved by obtaining a written opinion from the insurance company’s underwriter. Underwriters are generally the insurance company’s employees with the authority to contractually commit the company. If products liability insurance is needed, it will likely be necessary to acquire it from a different company than the company providing the general farm liability policy. For some value-added products, finding products liability coverage at all may be difficult.

Recall insurance may be needed in addition to products liability insurance. Products liability coverage does not include coverage for the costs of recalls. Recalls may be either voluntary or mandatory. Since most farmers and those in the marketing chain conduct recalls prior to a determination that the recall is mandatory, a policy that provides coverage for only mandatory recalls may not be what is needed. Where voluntary recalls are covered, it is important to understand what the events are that trigger coverage. Coverage for voluntary recalls is often hard to find. Many large buyers have clauses in their grower contracts that require the grower to indemnify the buyer for any costs of a recall. When discussing recall coverage, the insurance broker should have the opportunity to review these contractual provisions.2

2 Since many of these grower contracts are subject to nondisclosure agreements, it may be necessary for the grower to discuss the matter with her attorney prior to releasing the grower contract to the insurance broker.

Pooled processing facilities can solve the problem of unavailable products liability for some producers. These facilities have sufficient volume to purchase products liability insurance for all that produce products in the facility. They have also obtained the necessary licenses and inspections that insurers require. These facilities typically have waiting lists of producers that want to use the facilities.

Farmers may need to purchase workers compensation insurance to cover injured employees. In general, farmers may have more employees before carrying workers compensation insurance becomes mandatory than is the case for nonfarm employers. Workers compensation is a no-fault system designed to provide compensation to injured employees and families of deceased employees. Compensation is available for all work-related injuries and fatalities. There is no need to prove fault on the part of the employer. Compensation is provided according to a schedule established by each state. Farmers that are not required to carry workers compensation coverage may opt in. If the farmer does not opt in, then injured employees or the families of deceased employees must prove negligence. Any award granted by a court would be paid out of the farm’s general liability policy. Many farmers opt in because they find the certainty of the workers compensation schedule preferable to a catastrophic award that is possible in court in the tort system. The downside of obtaining workers compensation coverage is that it is expensive. Farming is always among the top two or three most dangerous job categories. Workers compensation coverage for farmers is priced to reflect the high level of risk. Employees covered under workers compensation may not choose to proceed in the tort system where a higher award beyond that offered in the workers compensation schedule can be obtained. An exception to this rule is where the farmer (employer) committed an act of gross negligence that caused the worker’s injury. In cases of gross negligence, punitive damages may also be available.

Figure 6.4 : Workers’ compensation, or employers’ liability insurance, is compulsory in some countries.

Farmers and others should always purchase title insurance when buying real property. If the farmer is financing the purchase of the property, she will likely be required to purchase lenders’ or mortgagee title insurance. This insurance protects the lender. The coverage diminishes until the loan is repaid, after which there is no coverage. Owner’s title insurance protects the purchaser of the property for as long as the purchaser or her heirs own the property and may even protect the insured after the insured has sold the property. It protects against covered claims against the property up to the policy limits and the cost of legal defense if the title insurer is required to defend the title.

Example 6.4. Farmer John purchased a new packing facility that included the land and the facility. Unbeknownst to John and his closing attorney, the seller of the facility had not paid the contractor who built the facility. John purchased owner’s title insurance with a policy limit of $1 million. The seller promptly took the money and himself to an unknown destination beyond the reach of the U.S. legal system. The contractor was owed $1.5 million. Within the statutory limit for filing a mechanic’s lien, the contractor made a filing putting his lien on record. That filing was after the closing date, so it was impossible for either John or his attorney to know of the lien prior to closing. The insurance company paid $1 million, with John on the hook for the remaining half million dollars.

Example 6.5. John Farmer typically stored his grain in three, 30,000-bushel grain bins. At a price of $4.75 per bushel, the value of the 90,000-bushels in storage was $475,500 and the total depreciated value of the bins was $25,000. Flooding from the Missouri River caused the grain to get wet and swell. The swelling grain destroyed the bins. The $25,000 value of the bins was covered under John’s property/ casualty policy. The value of the grain, $427,500, was neither covered under John’s property/ casualty coverage nor under his crop insurance. Property/casualty insurance that is part of a typical farm insurance policy generally does not cover stored grain. Crop insurance generally does not cover post-harvest events. John did not purchase a policy to cover the value of his stored grain. He was an unintended self-insurer.

There is other insurance needed by farmers. Health insurance is particularly problematic since buying this insurance in the individual private market is the most expensive way to buy it. If the farmer’s income is sufficiently low the farmer may qualify for a policy under the Affordable Care Act (Obamacare). Many farmers rely on coverage under an employer-sponsored plan that covers a spouse with an off-farm job.

Disability insurance is useful to provide income in the event that that a farmer is unable to work either temporarily or permanently. There is disability covered available automatically through federal Social Security; however, it does not provide coverage for short-term, temporary disabilities. Long-term care insurance is something farmers should consider as they may need coverage if they need skilled nursing care. Such coverage is expensive and the market for long-term care insurance is in flux because companies have experienced higher claims than anticipated.

Life insurance is important for farmers for a variety of reasons. Life insurance comes in many varieties of policies that are designed for different purposes. The basis distinction is between policies that provide only insurance (term insurance) and those that also contain an investment vehicle. Life insurance is tax-favored which makes it a useful tool for both retirement planning and estate planning. It can provide funds to bridge the gap caused by the death of a key member of the farm business. It can provide money for the care of minor children and a surviving spouse.

Managing insurance coverage

Managing insurance coverage is not simply a matter of picking the companies and policies that offer the lowest premiums. Here is a list of questions that one should ask in the process of managing their insurance coverage.

- Does the company adjust (resolve) claims quickly and fairly?

- Is your company, agents, or brokers easy to contact? Are they easy to contact in the event of an emergency?

- Are the agents or brokers that represent your company knowledgeable?

- Is your agent or broker willing to make a referral when their policy is not the best product for your needs?

- Does your company have resources that can help you manage your risks?

- Does your agent or broker speak respectfully of their competition?

- Does your company recognize your risk management efforts through lower premiums?

- What is the extended loss reporting period (TAIL) on your insurance policy?

- Is there any ‘grandfathered’ coverage in your current policy that is not available in new policies, e.g., has your carrier decided to quit writing new policies in your state?

- Does your policy cover environmental impairment liability?

- If you have a recall policy, what circumstances must exist to encourage coverage?

A key part of managing your insurance coverage is to analyze policy limits and deductibles, and the scope of coverage. A deductible is the amount the insured pays before the policy pays. Higher deductibles usually result in lower premiums. A deductible should not be so high that the insured has difficulty covering it.

A policy limit is the maximum amount that an insurance company will pay on a claim. Any amount above the policy limit is the loss of the insured. A common mistake, particularly selecting liability coverage, is to select coverage limits that are too low. In general, higher levels of coverage cost less on a per dollar basis than lower levels of coverage. If the coverage limits are too low, the insurance company may pay the coverage limit amount to the plaintiff and may be relieved of further obligation, including its duty to defend (depending upon policy language). The insured will then need to hire his own attorney for which he pays from his own funds. If the insurance company does not provide the additional insurance needed, the insured may need to purchase what is called excess liability insurance or an umbrella policy.

Analysis of the scope of coverage of one’s insurance policies is a critical part of managing insurance. It is an unhappy situation for an insured to be sued by a party claiming injuries and at the same time suing his insurance company over the scope of coverage. It is far better to determine the scope of coverage well prior to any need for the coverage. This requires a careful reading of the insurance policy and resolving any ambiguities. Policies are difficult for a lay person to understand. Attorneys involved in scope of coverage litigation have a saying, “What the twelve-point type giveth, the six-point type taketh away.” All ambiguities should be resolved by obtaining a written statement from the insurance company’s underwriter.

Example 6.6. Miller Joan decided to open a small retail feed sales operation next to her feed mill. Prior to this decision, she had only sold her cattle feed on the wholesale market to feed blenders. She inquired of her insurance agent, Klue Less, as to whether her retail operation would be covered under her existing general liability policy. Less said that he thought so. Not satisfied with that answer, she asked her son, an attorney, what he thought. He told her to ask Less to obtain a written answer to her question from the insurance company’s underwriter. The underwriter stated that the policy did not cover retail operations. Miller Joan purchased a rider to her policy that gave coverage for any liability arising from the retail operation.

Insurance coverage should be reviewed at least annually, and always when any major change in the business is planned. Any potential claim should be immediately reported to the insured’s insurance carrier. This is typically done by calling the insured’s agent or broker. The agent or broker will contact the insurance carrier that will ask the insured for any information that it requires.

Federal Crop Insurance Program (FCIP)

Federal crop insurance is delivered by private insurance companies that are paid by the United States to sell and service policies. The Federal Crop Insurance Corporation (FCIC), a wholly governmentowned corporation, was created by Congress to administer the FCIP. The USDA Risk management Agency (RMA) sets premium rates. As with Federal flood insurance there is no price competition in the federal crop insurance market. RMA engages in various ministerial duties that include:

- Administering subsidies for premiums and expenses,

- Approving and supporting insurance products,

- Managing the FCIC, and

- Providing reinsurance to private insurance companies.8

Federal costs in 2022 were $17.3 billion, of which $12 billion went to subsidizing premiums and the remainder was administrative expenses.9 As Congress has expanded the FCIP costs have increased.

Traditional crop insurance policies insure a single commodity.10 These policies fall into three categories:

- Yield-based policies that protect against a decline in yield without reference to price volatility,

- Revenue-based policies that are based on a decline in revenue (combine yield and price volatility), and

- Margin protection that protects against a decline in operating margin.

Policies are further defined by the indemnity trigger, i.e., the event that results in payment of a claim. Farmers and ranchers should understand what is being protected and whether that fits their individual risk management strategy prior to purchasing a policy. Often various options are offered to better fit the differing needs of producers.

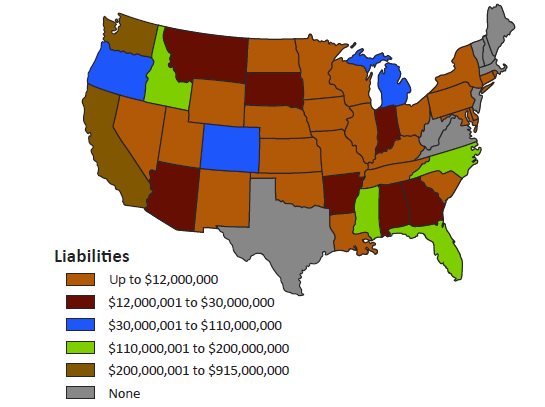

There are also policies that are not commodity specific. The Whole-Farm Revenue Protection (WFRP) provides protection for whole farming operations. There are also options for livestock producers for managing risks. These include Livestock Risk Protection, Livestock Gross Margin, and Dairy Revenue Protection. There are some supplemental policies and endorsements that can be added to traditional policies to provide more protection. That increases the cost of insurance. There is always the need to balance the additional cost of protection against the likelihood of a loss. It is also helpful to coordinate insurance with the benefits from commodity support programs where a producer is growing a supported commodity. Both private crop insurance agents and state Cooperative Extension can help with this analysis. Even though premiums are set by RMA, analysis is important to pick from among a variety of available insurance products. With a new Farm Bill expected to be enacted in 2024 it is likely that there will be significant changes to both the FCIP and commodity support programs.

Figure 6.5 : The Whole-Farm Revenue Protection (WFRP) liabilities by state

Parametric insurance

Parametric insurance11 is a new type of insurance that has not yet been seen in agriculture, except for certain supplemental policies introduced by RMA in the FCIP. Since it solves some of the problems associated with climate change, it will undoubtedly be used in agriculture. A parametric policy pays a specified amount of money when some parameter is met, e.g., the flood water level in a building rises to a certain level. Measurements can be made automatically by sensors in the building and payment can be made within days without the need for the services of an adjuster.

As can be seen from Table 6.1, all the supplemental policies introduced since 2015 rely upon specific calculations that do not require adjustment of any losses on the farmer’s farm. The basic policies that these policies supplement continue to require adjustment. Example 6.7 illustrates what an individual parametric policy for a corn farmer might look.

Example 6.7 HiTech Insurance has decided to offer a heat stress policy to Indiana corn farmers for the 2027 crop year. Ambient temperatures above 86 °F reduce corn yields. Hitech has developed an algorithm that uses days above 86 °F to determine the per acre payment. In return for a premium payment and the insured farmer’s agreement to allow HiTech to place sensors in her fields, HiTech will pay the insured an agreed upon sum for the number of days that the temperature is above 86 °F.

Rose Goslinga: Crop insurance, an idea worth seeding

How Does Insurance Work?

As can be seen from Table 6.1, all the supplemental policies introduced since 2015 rely upon specific calculations that do not require adjustment of any losses on the farmer’s farm. The basic policies that these policies supplement continue to require adjustment. Example 6.7 illustrates what an individual parametric policy for a corn farmer might look.

Example 6.7 HiTech Insurance has decided to offer a heat stress policy to Indiana corn farmers for the 2027 crop year. Ambient temperatures above 86 °F reduce corn yields. Hitech has developed an algorithm that uses days above 86 °F to determine the per acre payment. In return for a premium payment and the insured farmer’s agreement to allow HiTech to place sensors in her fields, HiTech will pay the insured an agreed upon sum for the number of days that the temperature is above 86 °F.

REFERENCES

11 U.S.C. § 109(b)(2) (2024, February 29). https://uscode.house.gov/view. xhtml?req=granuleid:USC-prelim-title11- section109&num=0&edition=prelim

16 U.S.C. § 3501, et seq. (2024, February 29). https://uscode.house.gov/browse/prelim@ title16&edition=prelim

Arias, E., Jiaquan, X., and Konchanek. K. (2023, November 7), United States Life Tables, 2021. National Vital Statistics Reports. https:// www.cdc.gov/nchs/data/nvsr/nvsr72/ nvsr72-12.pdf

FEMA. (n.d.). National Flood Insurance Program. https://www.floodsmart.gov/

Mims, C. (2023, December 9-10). How tech could save insurance. The Wall Street Journal. B2. https://www.wsj.com/business/ entrepreneurship/climate-change-aicalifornia- texas-insurance-1d993873

Morris, S. (2023, December 4). Crop Insurance: Update on Opportunities to Reduce Program Costs. U.S. Government Accountability Office. https://www.gao.gov/products/gao-24- 106086

Reinsurance News. (2023, December 19). Steve Evans Ltd. https://www.reinsurancene.ws/ tag/lloyds-of-london/

Turner, D., Tsiboe, F., Baldwin, K., Williams, B., Dohlman, E., Astill, G., Raszap Skorbiansky, S., Abadam, V., Yeh, A., & Knight, R. (2023). Federal Programs for Agricultural Risk Management. (Report No. EIB-259). U.S. Department of Agriculture, Economic Research Service. https://www.ers.usda.gov/publications/ pub-details/?pubid=108166

USDA Economic Research Service. (2019, August 20). Crop insurance. https://www.ers.usda. gov/agriculture-improvement-act-of-2018- highlights-and-implications/crop-insurance/

Wiles. R. (2021, October 29). Are Your Grains Protected? Blue Ridge Risk Partners. https:// www.blueridgeriskpartners.com/blog/agare- your-grains-protected

Endnotes

- Arias, E., Jiaquan, X., and Konchanek. K. (2023, November 7), United States Life Tables, 2021. National Vital Statistics Reports. https://www.cdc.gov/nchs/data/nvsr/nvsr72/nvsr72-12.pdf

- FEMA. (n.d.). National Flood Insurance Program. https://www.floodsmart.gov/

- Coastal Barrier Resources Act (CBRA) of 1982, as amended,16 U.S.C. 3501 (2023).

- Reinsurance News. (2023, December 19). Steve Evans Ltd. https://www.reinsurancene.ws/tag/ lloyds-of-london/

- 11 U.S.C. § 109(b)(2) (2023).

- Wiles. R. (2021, October 29). Are Your Grains Protected? Blue Ridge Risk Partners. https://www. blueridgeriskpartners.com/blog/ag-are-your-grains-protected

- 16 U.S.C. § 3501 (2023).

- USDA Economic Research Service. (2019, August 20). Crop insurance. https://www.ers.usda.gov/ agriculture-improvement-act-of-2018-highlights-and-implications/crop-insurance/

- Morris, S. (2023, December 4). Crop Insurance: Update on Opportunities to Reduce Program Costs. U.S. Government Accountability Office. https://www.gao.gov/products/gao-24-106086

- Turner, D., Tsiboe, F., Baldwin, K., Williams, B., Dohlman, E., Astill, G., Raszap Skorbiansky, S., Abadam, V., Yeh, A., & Knight, R. (2023). Federal Programs for Agricultural Risk Management. (Report No. EIB-259). U.S. Department of Agriculture, Economic Research Service. https://www.ers.usda. gov/publications/pub-details/?pubid=108166

- Mims, C. (2023, December 9-10). How tech could save insurance. The Wall Street Journal. B2.